USDT on Lightning Network offers emerging markets instant, low-cost payments with dollar stability. Discover how this combo solves banking access issues and currency volatility. See the future of global payments now!

The global financial landscape is rapidly evolving, with cryptocurrencies and blockchain technology playing an increasingly significant role. Among these innovations, stablecoins like USDT and scaling solutions like the Lightning Network have emerged as potential game-changers, especially for emerging markets. But could the combination of USDT on Lightning become the leading payment solution for these regions?

Emerging markets face unique challenges, including high transaction costs, limited access to banking infrastructure, and volatile local currencies. These issues have created a pressing need for innovative, affordable, and efficient payment solutions. Here USDT on lightning step up, a pairing that promises low-cost, high-speed transactions with the stability of a dollar-backed cryptocurrency.

In this blog we will explore the potential of USDT on Lightning to revolutionize payments in emerging markets, examining its advantages, challenges, and real-world applications.

The synergy between USDT and Lightning

By combining the stability of USDT with the speed and affordability of Lightning Network, this duo has the potential to revolutionize digital payments, precisely in the emerging markets.

Stablecoins like USDT eliminates the volatility associated with traditional cryptocurrencies, ensuring users can transact without worrying about price fluctuation. Meanwhile the lightning network enables instant, low-cost transactions, solving scalability issues that often plague blockchain networks.

Together, USDT and Lightning creates a seamless, cost-effective payment solution that outperforms traditional financial systems in speed, accessibility, and efficiency. This combination could drive financial inclusion, providing merchants and consumers in underserved regions with a borderless, stable, and efficient way to transact—potentially reshaping the global payments landscape.

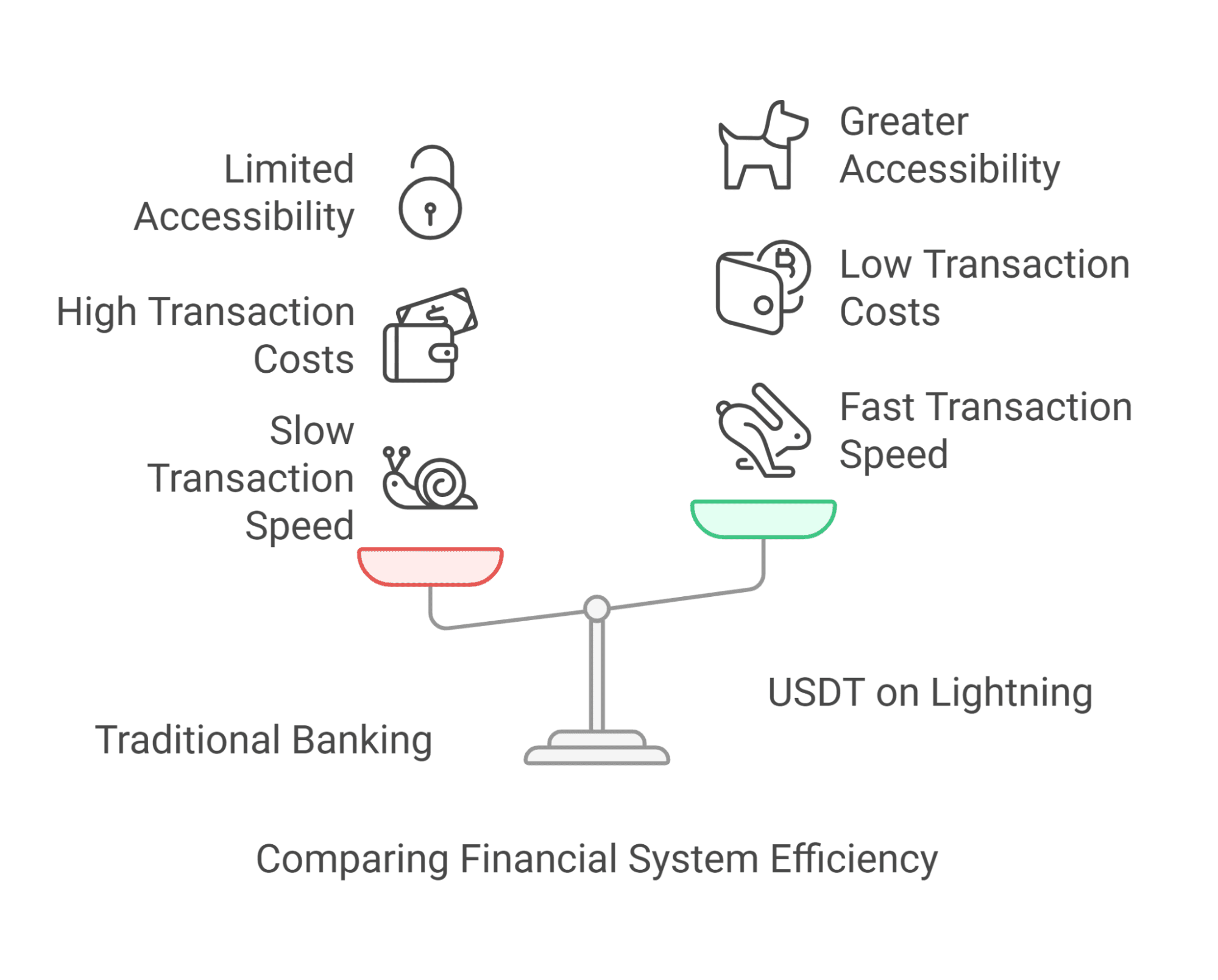

The challenges of traditional payment systems

When it comes to challenges of traditional payment there are certain areas of the emerging markets where it gets tough to go through using a fiat based system. These challenges are:

1. High transaction costs and fees

Traditional payment systems, particularly for cross-border remittances, impose high transaction fees that disproportionately affect individuals in emerging markets.

Whether sending money home to family members or making business payments, users often face hidden charges, unfavourable exchange rates, and intermediary fees that significantly reduce the final amount received.

For low-income earners, these excessive costs can erode hard-earned wages and make essential financial transactions burdensome.

2. Limited access to banking infrastructure

A significant portion of the population in emerging markets is unbanked or underbanked, meaning they lack the access to traditional financial institutions like banks. Factors such as geographic remoteness, lack of proper documentation, and high banking fees contribute to this exclusion.

Without access to basic banking services, credit, or digital payments, individuals and small businesses are forced to rely on cash-based economies, which are inefficient, insecure, and limit economic mobility. This lack of financial inclusion hinders entrepreneurship, investment, and long-term economic development.

3. Currency volatility and inflation

Many emerging markets experience unstable local currencies, with high inflation rates and unpredictable exchange rate fluctuations. This economic instability makes it challenging for individuals and businesses to save money, plan for the future, or engage in international trade.

Rapid currency devaluation can lead to loss of purchasing power, increased cost of imports, and economic uncertainty, further exacerbating financial insecurity. Without access to stable financial alternatives, people are left vulnerable to economic shocks, making it difficult to break out of poverty cycles.

Together these challenges highlight the urgent need for alternative, cost-effective, and inclusive financial solutions that empower individuals and businesses in emerging markets.

Why USDT on Lightning could be a game changer?

1. Low-cost, high-speed transactions

The Lightning Network is designed for instant, near-zero-fee transactions, making it one of the most efficient solutions for digital payments. Unlike traditional payment processors, the Lightning Network enables settlements in seconds. When combined with USDT, which eliminates the volatility associated with other cryptocurrencies, this creates a payment method which is ideal for new players.

This pairing has the potential to become a mainstream crypto payment processor for businesses and consumers worldwide, offering an alternative to expensive and slow legacy financial systems.

2. Financial inclusion

One of the biggest barriers in emerging markets is the lack of access to traditional financial services. USDT on lightning removes this hurdle, allowing anyone with a smartphone and internet connection to send and receive payments instantly. There’s no need for a bank account, making it an ideal solution for unbanked populations.

With this technology, businesses and individuals can transact globally without intermediaries, unlocking new economic opportunities and fostering financial independence.

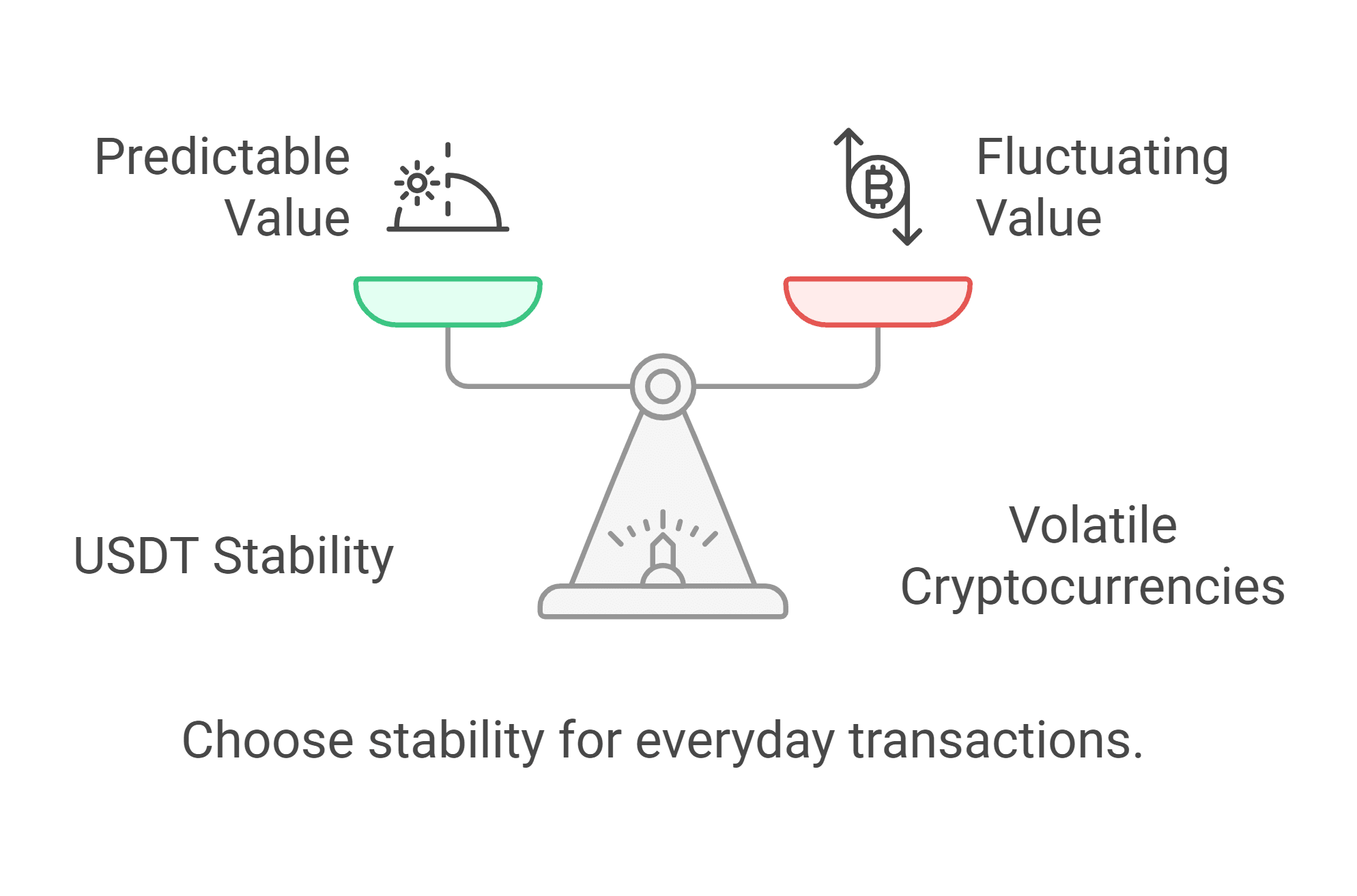

3. Stability

Many countries struggle with currency devaluation and inflation, eroding the purchasing power of their citizens. USDT is pegged to US dollars, provides a stable store of value, protecting users from extreme price fluctuations in local currencies.

By integrating USDT with instant settlement capabilities users gain a reliable, and accessible financial tool to store and transfer value. This makes it a practical solution for everyday transactions, savings, and cross-border payments in unstable economies.

Together, USDT on Lightning delivers a powerful combination of speed, affordability, accessibility, and stability, making it a potential game-changer for global payments and financial inclusion.

Real-world use cases and potential applications!

Cross-border remittances

Remittances are a lifeline for millions of families in emerging economies, often representing a significant portion of their income. However, traditional remittance systems are plugued by high fees, slow processing times, and limited accessibility.

USDT on lightning can revolutionize this space by enabling instant, cross border transfers.

For example, a worker in the United States could send money to their family in the Philippines in seconds, with fees as low as a fraction of a cent.

This not only saves money but also ensures that funds are delivered quickly, even in urgent situations.

Peer-to-peer payment

In everyday life, people frequently need to send money to friends, family, or colleagues—whether it’s splitting a restaurant bill, paying rent, or reimbursing a friend for a favor. Traditional methods like cash or bank transfer can be inconvenient or costly.

USDT on Lightning makes peer-to-peer payments fast, easy, and affordable.

For instance, two friends could split a $50 bill by sending 25 each via a lightning-enabled wallet in seconds.

This ease of use makes it a reliable crypto payment processor for everyday transactions.

Merchant adoption and E-commerce

For businesses, especially small and medium-sized enterprises (SMEs), accepting payments quickly and cost-effectively is crucial. High transaction fees and slow settlement times can eat into profits and create cash flow challenges.

USDT on Lightning provides a solution by enabling instant, low-cost payments for both online and offline purchases.

For example, a coffee shop in Nigeria could accept USDT payments via the Lightning Network, allowing customers to pay for their orders in seconds.

Similarly, an e-commerce platform could integrate USDT on Lightning to offer a seamless checkout experience for customers worldwide.

Advantages over competing solutions

USDT on Lightning vs. Traditional banking

USDT on Lightning vs. Other cryptocurrencies

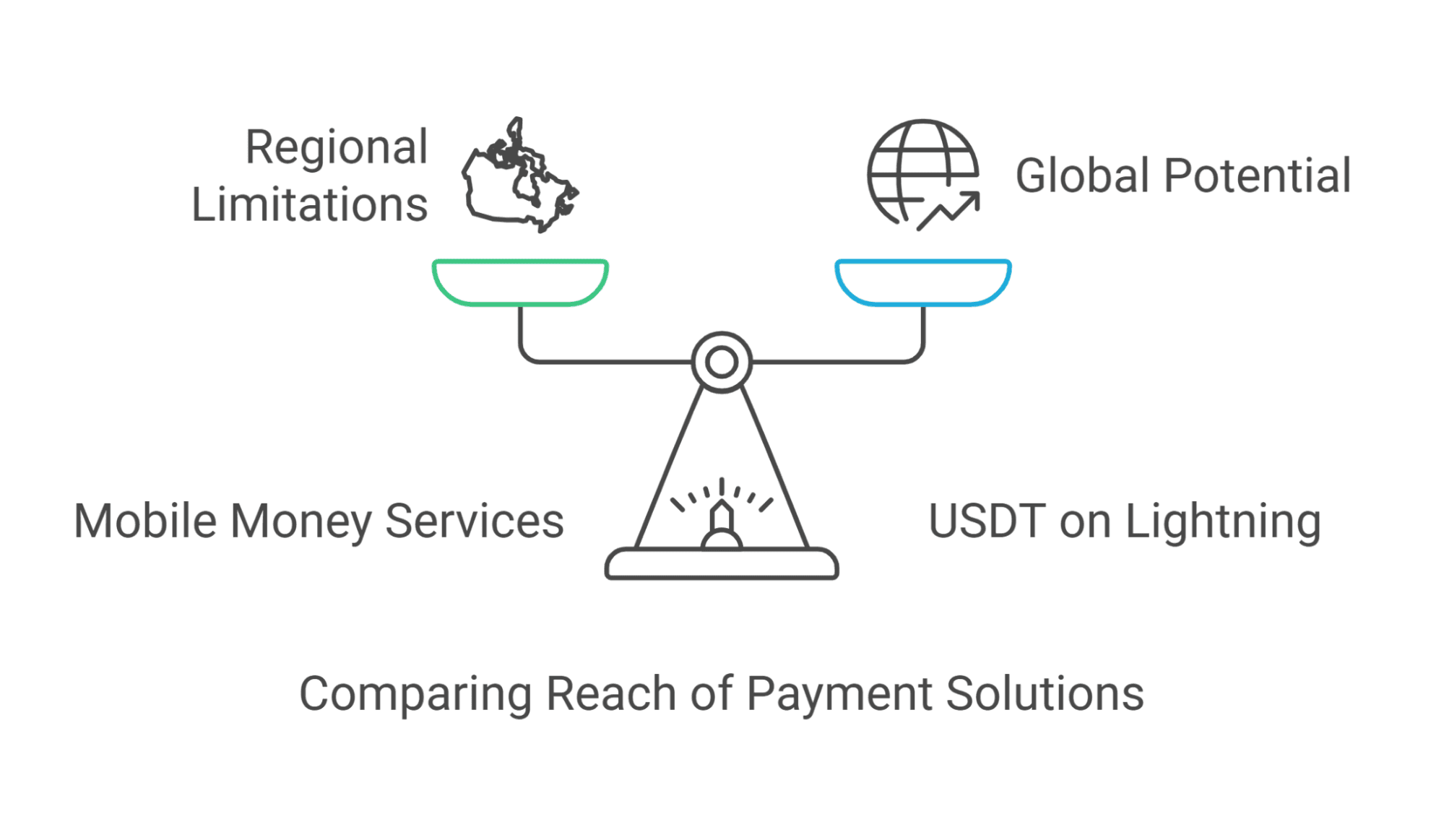

USDT on Lightning vs. Mobile money services

The role of emerging markets in shaping the future of payments

Emerging markets are not just beneficiaries of financial innovation—they are often its driving force. Out of necessity, these regions have become hotbeds for creative solutions to longstanding challenges like high transaction costs, limited banking access, and currency instability. The adoption of USDT on Lightning in these markets could play a pivotal role in shaping the future of global payments. Here’s how:

1. How adoption could drive global change?

Emerging markets are home to billions of people who face significant barriers to accessing traditional financial systems. This has created a fertile ground for alternative solutions like USDT on Lightning to thrive.

Necessity breeds innovation: In regions where traditional banking is inaccessible or inefficient, people are more likely to adopt new technologies that offer tangible benefits. For example, in countries with high remittance costs, USDT on Lightning provides a faster, cheaper alternative that directly addresses a critical need.

Scaling through adoption: As more people in emerging markets use USDT on Lightning, its network effect grows. Increased adoption leads to greater liquidity, more merchant acceptance, and improved infrastructure, making it a viable leading payment solution not just locally but globally.

Influence on global trends: Emerging markets often set trends that ripple outward. For instance, the success of mobile money services like M-Pesa in Africa has inspired similar innovations worldwide. Similarly, the widespread adoption of USDT on Lightning in these regions could encourage its acceptance in developed markets, establishing it as a global standard.

2. Lessons from early adopters

Countries and communities that embrace USDT on Lightning early will serve as test cases for its potential, providing valuable insights and best practices for others to follow.

Real-world proof of concept: Early adopters can demonstrate the effectiveness of USDT on Lightning in solving real-world problems. For example, a country experiencing hyperinflation could show how USDT’s stability combined with the Lightning Network’s speed can protect savings and facilitate commerce.

Building best practices: As these pioneers integrate USDT on Lightning into their economies, they will develop strategies for overcoming challenges like regulatory hurdles, technical barriers, and user education. These lessons can be shared with other regions, accelerating global adoption.

Driving innovation: Early adopters often push the boundaries of what a technology can do. Their unique use cases—whether it’s enabling microloans, facilitating cross-border trade, or powering decentralized marketplaces—can inspire new applications and innovations.

Conclusion

The combination of USDT on Lightning represents a transformative solution to some of the most pressing financial challenges faced by emerging markets–and beyond. By leveraging the stability of USDT and the speed and affordability of LN, this pairing offers a powerful tool to address issues like high transaction costs, limited access to banking, and currency volatility.

While challenges such as regulatory hurdles, technical barriers, and user education remain, the benefits far outweigh the risks. As adoption grows, USDT on lightning has the potential to redefine the global payment landscape, making it faster, cheaper and more inclusive.

In essence, USDT on lightning isn’t just a technological innovation—it’s a catalyst for economic empowerment and financial inclusion. As more people and businesses embrace this solution, it could pave the way for a more connected, equitable, and efficient financial system worldwide.